You are the Chief Risk Officer or the Head of “Economic capital and Strategy” of your financial institution ?

ALGOSAVE CAPITAL SAVING platform is a tool that lets you easily gain powerful insights into issues of credit dependencies in your financial asset portfolio. It will even allow you to see how LOW default correlation actually is, compared to sky-high CDS correlation. Use ALGOSAVE CAPITAL SAVING PLATFORM to SAVE capital and improve RAROC assessment.

Download this use case : here.

1 – From capital saving…

We, bankers – and I used to be one – have been caught with our hand in the low correlation cookie jar. We decided to take action so that it won’t happen again.

To add to our comfort – or rather, discomfort really – markets are confirming our fears and react exactly this way . Looking at CDS prices one could even ask : why bother having one CDS per issuer ? Let’s just have one CDS per industry. One size fits all !

For example, the first CDS 5-year graph is that of Royal Dutch Shell (RDSA), the second one is that of Total SA, and the third one is that of Statoil (renamed Equinor).

Kudos to https://www.datagrapple.com/ for those graphs

Guessed the 85% correlation ?

Immediate consequence : in stress-test scenarios, banks must take into account this thru-the-roof – 85% – CDS implied Probability of Default correlation and put aside a lot of capital.

Why ? since defaults of rock-solid corporates – such as the one we just looked at – are very rate events, there are very little statistics of actual default contagion in high grade credit portfolios.

So, in order to measure default contagion, lenders are left using whatever proxy they can find. But, although CDS – or share, or bond – price correlation is the most obvious one, at 85% it is also a killer !

BUT, let’s look back in the past and ponder about bankruptcies of large corporates : Enron, Worldcom, General Motors. Can we say that, as their CDS correlation predicted it, 80% of the best and most solid Telecom, Energy and Automotive corporates have been wiped out ? NO

The only industry where this default correlation holds true is the heavily regulated financial industry. Probably because it is … regulated.

But in all other industries, and as any experienced CLO trader will tell you, default correlation is markedly lower than CDS correlations. Even – and especially – in crisis regime.

Confirming this feeling, ALGOSAVE CAPITAL SAVING shows exactly that even in stress-test scenarios, default correlation is actually far lower than CDS thru-the-roof correlation suggests. And it is definitively worth our while and that of our clients.

Here is an example on our favorite Integrated Oil and Gas portfolio.

For instance, whereas Total/RDSA 5-year CDS correlation is close to 85%, ALGOSAVE shows that it is actually closer to 21% even with a stressed macro-economic scenario. Granted, it is still more that 10 times TotalSA/RDSA conditional default probability in consensus OECD macro-economic scenario. But it is a far cry from the 85% CDS correlation mark.

Well done, from 85% down to 21% default correlation that’s tangible capital saving. If not directly, at least thru far less pro-cyclical capital requirement which – in itself – is a blessing in disguise.

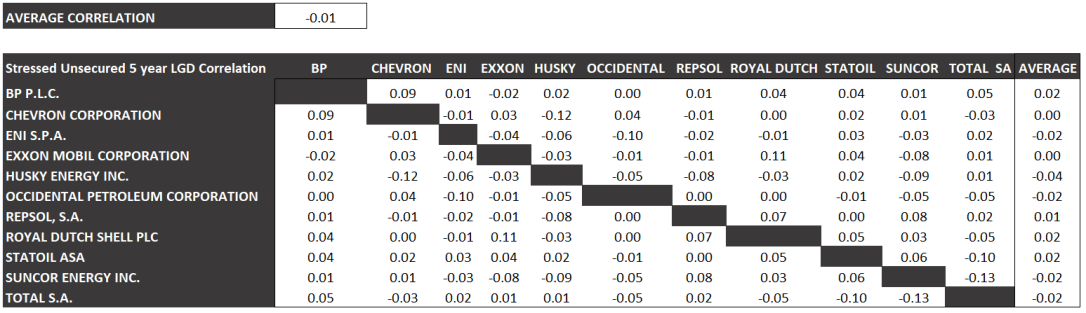

ALGOSAVE proprietary ISSUER DATABASE is full of those CAPITAL SAVING nuggets, and some others too. Such as Loss Given Default correlations which also hold an interesting capital saving surprise. Indeed, LGD correlation is also lower than current credit model suggest. Frankly, how could it be otherwise since , to the notable exception of the heavily regulated financial industry, corporate degree of financial leverage it THE main decision left to CFOs to increase ROE. Indeed, sales margin is mostly a function of technology and asset turnover is mostly determined by the competitive landscape of the corporate.

We actually dig into this phenomenon in greater details in this post here..

2 – to improvement in RAROC assessment

We also think that ALGOSAVE FinTech will be the source of a dramatic improvement in RAROC assessments. Indeed, by providing appropriate forecasts of Default Probability, Point In Time credit ratings, issuer and seniority specific Loss Given Default, Expected Losses and their related correlation, ALGOSAVE provides the much-needed forward looking parameters as well as the dynamics required to produce proper forecasts and deliver a robust pricing decision support system.

Ask for your private access to ALGOSAVE CAPITAL SAVING PLATFORM, check those credit dependencies, improve RAROC assessment and start SAVING Capital now.